Top 3 Nomura Global Markets Interview Questions

Last Updated:As I've written about before, it's always a good idea to join a bank - all else being equal - where sales and trading is a valued and significant division.

For Nomura this certainly holds true. In fact, their Q2 2022 financial results revealed that while most areas of Nomura's business suffered a downturn - from investment banking to retail banking - their sales and trading operation was able to pick up the slack and help produce a profitable quarter for the bank. As Michael Makdad of Morningstar put it when discussing the quarterly results, "Everything looks lousy except for fixed income trading".

The reality for every large bank is that volatile markets will tend to reduce merger volumes and produce outsized loses within retail banking. However, within sales and trading divisions volatile markets are generally a good thing - as long as they don't get too volatile - as heightened market volatility generally leads to more trading activity from clients and wider spreads.

In this post I'll do something similar to what I've done during the past few months: provide answers to questions surrounding broader market themes that are happening right now. Given how volatile, fast-paced, and uncertain markets are right now, it's likely most helpful to give you a sound perspective that you can utilize during interviews. Indeed, it was only a few months ago when I was walking through what a 2s10s yield curve inversion meant and anticipating that we'll likely see it (although I had no idea the inversion would occur so quickly or get so deep for a period of time).

Nomura Global Markets Interview Questions

Nomura has followed the same script as many other banks in rebranding their sales and trading business "global markets". It all means the same thing and Nomura has always been quite strong - in particular in APAC - in the world of fixed income trading (especially in rates).

What has been driving yields in the US over the past few weeks? What has changed?

The 2s10s spread is currently inverted. Do you think it will continue to be?

Given the instability in Europe, why is the ECB planning to aggressively raise rates?

What has been driving yields in the US over the past few weeks? What has changed?

With the hot CPI and PCE prints occurring in May and June, yields dramatically rose in the front-end of the yield curve in anticipation of the Fed needing to embark on an even more aggressive and sustained rate hike cycle than was previously anticipated.

However, through July and August things changed: CPI appeared to have peaked, University of Michigan inflation expectation surveys came in weaker than expected, significant declines in commodity prices occurred, and there appeared to be a modest hint of labor market softness creeping into the data.

This then led, as you likely know, to a rapid reversal in yields across the curve (but in particular in the front-end). If you look at the two-year yield, you had a rapid ascent to 340bps on June 13th before falling down to ~290bps by the end of July. While half a percent may not seem like a large decline, in the world of treasuries it represented a massive reversal in a short period of time and signalled that market participants were no longer anticipating the Fed needed to raise rates as aggressively to tame inflation.

In other words, a soft landing was becoming viewed as more likely by the market given that monetary policy wouldn't have to become as restrictive as previously thought. Based on this assumption, risk assets ranging from equities to crypto began to surge with the NASDAQ going up 23% from mid-June to late-August.

This was most certainly not welcome news for the Federal reserve. Yields coming down and risk assets rallying is a sign of financial conditions loosening, which is exactly the opposite of what the Fed is trying to accomplish through rate hikes. And, of course, this was all occurring while inflation was still at 40-year highs without having come down meaningfully.

Based on this, Chair Powell decided he needed to throw cold water on what he was seeing: making it clear that the mistakes of the 70s - when Chair Arthur Burns would let off the brakes whenever inflation appeared to be trending down, only to then have it rise again - would not be repeated by him. This is exactly what he used his speech at Jackson Hole to do.

Chair Powell's speech had the predictable effect of causing equity markets to sell off significantly and for a repricing of the yield curve to occur over the following weeks. With recent data showing job openings ticking back up (after falling in previous months) and jobless claims falling, this has only added fuel to the fire.

It's now become clear to most market participants that in order for inflation to be tamed and brought back down to 2% there will need to be, as I've said in other posts, some level of labor market pain and that simply has not occurred yet.

Take a look at the Fed Funds expectations for December of 2022 below. As you can see, markets have moved up their rate hike expectations back inline with what the consensus view was back in June.

The 2s10s spread is currently inverted. Do you think it will continue to be?

As I've written about in the past, the 2s10s spread has recently inverted to quite negative levels. In fact, at one point the inversion reached levels that were even more negative than were observed during the Great Financial Crisis.

The reason why you'll hear some market participants and many in the media talk about the 2s10s spread is because it's a reasonably reliable recession indicator. When the 10-year treasury is significantly lower than the two-year treasury what the market is basically saying is, "We think that rates will be high in the short term, but will need to be reduced shortly thereafter because of a recession beginning, which will then require the central bank to cut rates in order to stimulate growth."

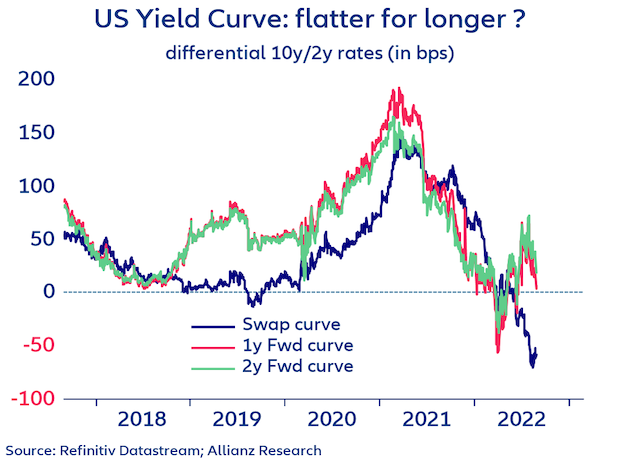

Interestingly, you can look at where the 2s10s spread is in future years by looking at one-year, two-year, etc. forward swaps. What this allows you to see is whether the market, in future years, expects the yield curve to flatten or steepen out. What this would signal is that the central bank has, in future years, reduced rates such that the front-end is no longer higher than the long-end (or, alternatively, that the economy has escaped recession and is back growing again so the yield curve has regained a normalized slope).

Anyway, here's a chart showing the current 2s10s spread and what it is projected to be one-year and two-years out. What this shows is that the market is anticipating the mid-section of the yield curve to be almost completely flat over the next few years (in other words, the two-year and the ten-year yield being roughly the same).

As you can see, in the past few months (when yields were falling and equities rallying) the market anticipated that there would actually be a bit of steepness to 2s10s in future years. The reason why is that the prevailing market narrative over the past few months - which never made much sense to me - was that the Fed would aggressively raise rates through 2022 and then begin cutting rates in 2023 as soon as inflation began to fall significantly and the economy softened. So, the market thought the Fed would pivot quite soon.

However, surrounding Jackson Hole the rhetoric coming out of the Fed shifted market sentiment heavily as the Fed members made it clear they were interested in holding rates "higher for longer". So, now the market realizes that it's more unlikely that the Fed will be cutting rates in 2023 even if there is significant softness in the economy. Rather, it's likely that the Fed will keep rates high until it sees inflation approaching something like normal (maybe 3-4%) in a rapid and unequivocal manner.

In other words, the Fed has finally explicitly acknowledged that some level of economic pain - through sluggish growth and higher unemployment - is a necessary ingredient to getting inflation down, and they're willing to make that tradeoff.

Therefore, the reason why the market is now anticipating a flat or maybe even negative 2s10s spread in the future is because they see a sluggish economy and the need for the Fed to lower rates in the future, but they are now recognizing that won't likely come as soon as they previously thought (as the Fed is committed, at least rhetorically, to holding rates high until inflation comes down to around their target).

Note: Here's a snapshot of how inverted the yield curve is as of late-2022. It's currently the most inverted in the past forty years, which is a consequence of the Fed undertaking the most aggressive rate hiking cycle of the past forty years and predictions for slower economic growth into 2023 and 2024 (which the market is thinking will lead to future rate cuts).

Given the instability in Europe, why is the ECB planning to aggressively raise rates?

The market is currently pricing in that the ECB will raise rates by 75bps at their next meeting and make significant rate hikes at subsequent meetings. This would have been something no one would have believed even just three months ago, as members of ECB have been notoriously dovish relative to their counterparts at the BoE and the Fed.

The radical change of heart comes down to a few different factors:

First, inflation data has been coming in much higher than anticipated. If this inflation were strictly coming from higher energy prices then this data wouldn't have raised as many alarm bells. But what recent data has shown is elevated core inflation that is troubling due to how "sticky" core inflation tends to be.

Second, inflation forecasts for 2023 have steadily marched up and are now at a staggering 4.2%. This is troubling because inflation tends to be a bit of a self-fulfilling prophecy. If people believe there will be significant inflation in the future, they will take actions (i.e., demand higher wages, raise the price of good, etc.) that contribute to elevated inflation in the future.

Third, this level of heightened inflation - matched with very low rates - has led to the Eurozone having remarkably negative real rates (nominal rates adjusted for inflation). This has been one of the factors, along with the energy crisis, that has led to the Euro weakening against the dollar so significantly (as of this writing, the Euro has broken parity and is now worth less than the dollar).

This currency weakness then helps feed inflation as suddenly importing dollar denominated goods costs more (in Euros) which then needs to be passed on to consumers. The quickest and surest way to get the value of the Euro back up is to raise rates which will then help reduce inflationary pressure coming from the weakening currency (if you're curious about how rates inform FX levels, check out the FX Sales and Trading Guide in the members area). Raising rates also will, obviously, have the affect of cooling the economy which helps lower inflationary pressures coming from the demand-side as well.

The reality is that the ECB is in an almost impossible bind. Nearly every investment bank is officially forecasting an upcoming recession in the Eurozone and the exchange rate has seen a significant decline relative to most major currencies. Added on top of all of this is, obviously, an energy crisis with no easy solutions (personally, I don't think the unfolding energy crisis is even fully "priced in" yet).

However, to answer the initial question here: given how much inflationary pressure there is in the Eurozone - coming from all directions, including from currency weakness - the ECB has no choice but to try to raise rates as much as possible and to do so as quickly as possible. This will hopefully help tame inflationary pressures as much as possible and then give the ECB some room to cut rates in the future to spur economic growth if a meaningful economic contraction takes hold in the next year.

Conclusion

It hasn't been this interesting of a time in fixed income since the Great Financial Crisis (with the exception of possibly the Eurozone Crisis in 2010 if you happened to be based in Europe).

Fortunately, fixed income sales and trading has always been a strong area of Nomura and their recent financials highlight how this is more true than ever today. With that said, Nomura does run a rotational internship program so you'll be able to get some exposure across asset classes in different capacities (sales, trading, and research).

Anyway, hopefully you've enjoyed this post. We covered topics in a bit more depth than you'd ever be expected to give in an interview - whether at Nomura or at any other bank - so don't worry about needing to memorize everything here.

However, I've gotten a number of e-mails from people that say they really enjoy when I dive a bit deeper into current happenings in the markets, so hopefully you've enjoyed these questions and answers. If you're looking for more interview-style questions, you should read the nineteen sales and trading interview questions I put together as well.