Gilt Volatility and the Return of Quantitative Easing: What it All Means

Last Updated:The past few weeks have seen some unprecedented volatility hit long-dated gilts. Indeed, the volatility reached such an extreme toward the end of last month - driven by quite idiosyncratic factors we’ll get into later on – that the BoE started a narrow, time-limited form of quantitative easing in order to stop the spiralling upward of yields out the long-end of the curve.

Restarting quantitative easing – even if the intent behind it is quite different than in past episodes – has a grim form of irony because the BoE had initially been planning to start their quantitative tightening program this month. Instead, the tightening will (allegedly) begin on October 31st, two weeks after the end of the current quantitative easing that’s occurring.

But let’s not get ahead of ourselves too much here. What has been occurring in the UK over the past few weeks has weighed heavily on global markets – especially in rates – as folks try to disentangle whether what’s happening in the UK is entirely unique to them and, even if so, what spillover could eventuate from further gilt volatility.

Given that sell-side research coming from GS, JPM, Barclays, etc. over the past few weeks has been dominated by these questions, it’s obviously impossible for me to give you a comprehensive overview in just this post.

Instead, I’ll be giving you some background resources on what's happened and talking through the most interesting aspects of what’s going on from a sell-side perspective (i.e., explaining how what the BoE is doing is only quantitative easing in the literal sense of the word, and does not constitute an explicit policy pivot as some market participants were hoping in vein for).

How The Gilt Market Reached a Crisis

Fortunately, how we got here can be told in a pretty linear way. I’ll provide a day-by-day breakdown below, but for a more full-throated explanation, read through the excellent Bank of England report sent to Parliament regarding the actions they took and what led up to them. It's an extremely well-crafted report that's just eleven pages, so well worth reading in full.

Friday, September 23: The UK’s Mini-Budget and Mini Shock

Markets in the UK were relatively subdued prior to the new conservative government’s release of their mini-budget. While much of the mini-budget was well forecast before being officially announced, certain fiscally expansionary measures weren’t (such as a tax cut for top earners, which have since been reversed.

During the day, the market had a reaction that is largely along the lines of what you’d expect: sterling sold off, in particular against the USD, and yields rose in anticipation that the BoE would need to do more hikes to tame inflation given the fiscal expansion that will be occurring from the budget. Importantly, the selling was orderly and nothing too worrisome.

However, after the announcement was made The Chancellor of the Exchequer then did a series of interviews saying this was just the beginning of what was to come. Making it clear that fiscal expansion was here to say, despite the UK being in an inflationary environment in which the BoE has been consistently more dovish than the Fed due to how over-levered households are with floating-rate debt.

This is what really led to the sell-off Friday, which reverberated through the weekend. GBP/USD sold off 4% and long-end gilt yields rose 30bps in very illiquid conditions. By the end of day on Friday, storm clouds were forming.

September 24 to September 27: The Aftermath

On Monday, the 26th, the sell-off in both FX and rates continued to accelerate with long-end gilt yields rising another 50bps. This was then followed by extremely volatile trading on Tuesday with long-end yields ending up another 50bps.

It was clear to all institutional market participants that this was not a sell-off driven purely by fundamentals (i.e., being driven purely by the fiscal expansion that would be occurring due to the new budget). There was clearly forced selling occurring due to a technical issue of some kind, and that this forced selling was occurring during a period of deep illiquidity in what should be quite liquid markets (thus why the moves each day were so large).

Here are some great charts from the BoE itself illustrating the incredible FX and rates moves that occurred over the course of just a few days…

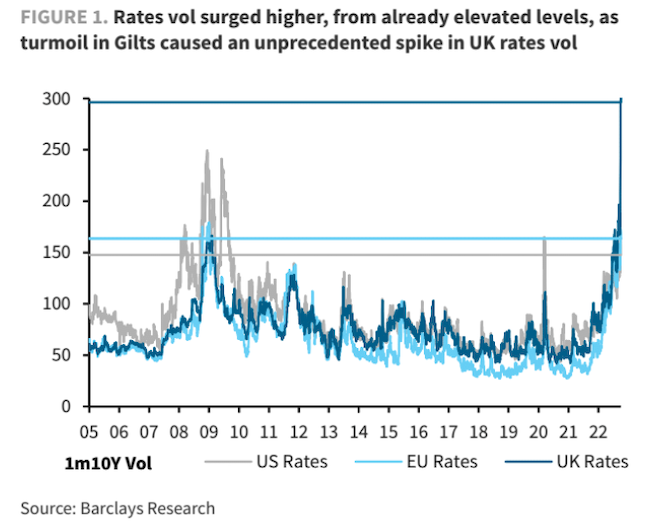

In case you were wondering just how volatile things got, and how this volatility stacks up to past periods of volatility, look at this chart I’ve pulled from a Barclays research note from last week…

September 28: The BoE Intervention

On Wednesday, the 28th, the BoE stepped into the void recognizing that yields would continue to spike due to forced selling, thus creating a dangerous spiral (as we’ll get into in the next section). The aim of the BoE was to try to beat back the yields on long-dated gilts, as long-dated gilt price declines were creating the collateral (margin) calls that forced the selling of long-dated gilts by certain types of market participants, which then caused more gilt price declines, etc.

So, what the BoE did is announce that they’d be stepping in to purchase long-dated gilts. Their initial announcement had a “we’ll do whatever it takes” tone to it, but in reality the program was time-limited and funding-constrained.

From September 28th to October 14th, the BoE announced they would purchase up to £5bn of gilts a day (or £65bn in total) in order to provide the market with liquidity. The mere fact that the BoE was stepping in immediately caused long-dated gilt yields to tumble by over 100bps on the 28th. Thereafter, yields stayed relatively range bound for the rest of the week and into the start of the week after.

So, here’s what the BoE was really trying to do with this operation. They recognized that the gilt turmoil happening out the long-end of the yield curve was being caused by a specific issue related to pension funds that were getting collateral (margin) called. As they were getting margin called, they dumped long-dated gilts, which caused the prices of long-dated gilts to go down further (exacerbated by terrible liquidity and few buyers in the market) that then forced more margin calls.

This vicious cycle created an incredible amount of volatility that is only loosely tied to fundamentals. While true that it wouldn’t have happened without the mini-budget, it’s unfair to say it’s directly caused by the mini-budget. Rather, it's perhaps better to say that the mini-budget was a match thrown onto an already present oil spill.

So, the BoE recognized that by stepping in and getting long-dated yields down this would temporarily stop the margin calls and give market participants (pension funds / LDI funds) the ability to have the time to (hopefully) unwind their positions in a more orderly fashion and stop the financial instability that they were causing by their forced selling. Further, this would prevent any of these funds from really blowing up or market liquidity to entirely vanish.

Now many - especially in the financial press - clamored to say that the BoE was restarting quantitative easing and that this constituted a major central bank capitulating to markets and pivoting, but this isn't the right framing to use.

The purpose behind traditional quantitative easing – as it was done during the financial crisis and the pandemic – is to create looser financial conditions by reducing the long-end of the curve and therefore hopefully stimulating demand.

While this operation is quantitative easing – using the literal sense of the phrase – since it involves the buying of securities by a central bank, the intent behind this operation is fundamentally different than in the past: the BoE doesn’t want to create significantly looser financial conditions (that’s why they have been raising rates, and have made sure to say they will continue to!). Rather, they recognized there was a specific technical issue creating financial instability in a part of the market and sought to rectify it before it got any worse.

As you can see from the Goldman chart that I pulled for you below, they were successful through the first week in stemming volatility and putting a temporary cap on yields (which you can see by virtue of the fact that they’ve had to step in to buy very few long-dated gilts – it remains to be seen if this will continue after they withdraw support though…).

And here's an illustration from Barclays of just how wildly the yield curve shifted during a very short period of time...

Liability-Driven Investment (LDI) Funds and their Issue

At the heart of the long-dated gilt turmoil are pension funds. While this may sound a bit surprising – given that pension funds are often viewed as being sleepy and conservative – that’s exactly why it shouldn't be surprising!

There are few natural buyers of long-dated gilts. But for pension plans that, by definition, have long-dated obligations they must meet, having risk-free assets that can provide significant duration makes sense. However, given how low yielding gilts have been since the financial crisis – along with some accounting nuances – liability-driven investment funds began to be utilized that have the sole purpose of trying to give pension funds liability-matching (from a duration perspective) exposure to gilts (often on a levered basis, to boost returns).

Anyway, this is an incredibly quick overview of the situation. The best overview of how LDI funds helped spur the gilt turmoil is provided by the Bank of England report referenced earlier. Here are a few quick quotes from the above report that will explain what’s going on here…

Here’s the BoE’s definition of LDIs…

“LDI is an investment approach used by defined benefit (DB) pension funds to help ensure that the value of their assets (i.e. their investments) moves more in line with the value of their liabilities (i.e. the DB pensions they have promised to pay in the future). The approach is intended to achieve a smoother, more certain path to fully funded status. The closest match for the risks around the value of the liabilities is long-term gilts, particularly those linked to inflation. LDI strategies have been employed for many years.”

Here's how LDIs work…

“LDI strategies enable DB pension funds to use leverage (i.e. to borrow) to increase their exposure to long-term gilts, while also holding riskier and higher-yielding assets such as equities in order to boost their returns. The LDI funds maintain a cushion between the value of their assets and liabilities, intended to absorb any losses on the gilts. If losses exceed this cushion, the DB pension fund investor is asked to provide additional funds to increase it, a process known as rebalancing. This can be a more difficult process for pooled LDI funds, in part because they manage investment from a large number of small and medium sized DB pension funds.”

Here's why the BoE felt the need to intervene…

In case you're curious, here's a brief history of LDIs from the Financial Times.

Where We Are Today (Is the Gilt Turmoil Done?)

As illustrated earlier with the screenshot of a GS research report, the operation was a success in terms of bringing down yields immediately – thus stopping the vicious margin call cycle – while also not needing to have the BoE actually make many purchases.

Over the past week and especially over the past few days, long-dated gilts have risen in a reasonably orderly but quite aggressive manner. This in and of itself isn’t much of an issue – the BoE is likely fine with long-dated gilts rising to 470bps or even 500bps so long as it doesn’t cause undue financial stress in the process (as was the case when they rose from 350bps to 490bps from Sept 19-27!).

This again gets to the distinction between this form of “quantitative easing” and more traditional forms we’ve become accustomed to: this one was all about creating market stability and giving breathing space to pension and LDI funds to hopefully unwind any excessively levered positions they have (insofar as they can). In other words, if yields readjust to where they were prior to the intervention by the BoE, but it occurs in an orderly way without creating financial instability, that isn’t per se an issue to the BoE.

However, the issue everyone is grappling with today is whether or not yields skyrocket again once BoE support is withdrawn – or whether the BoE is tested later this week before withdrawing support. Put more simply: has all the excessive leverage that caused the gilt turmoil really been drained or can it really be drained?

Earlier today (Tuesday, October 11) the BoE announced it’d widen the scope of daily gilt purchases by opening up a new sleeve of £5b per day to provide a backstop to the inflation-protected gilt market after yields spiked significantly in that market yesterday (yields also rose sharply on thirty-yield gilts yesterday, at one point being up ~35bps). So now there’s £10b in daily purchasing power for the BoE: £5b for index-linked gilts and £5b for regular-way gilts.

The reason for the inflation-linked gilt intervention is the same as for the original intervention on long-dated gilts: a vicious circle was causing yields to spike upwards due to forced selling by defined benefit pension funds (who are the by far the largest buyer of inflation-linked gilts).

Here’s a good article from the Financial Times about the intervention today, along with a chart showing just how unprecedented the volatility is right now in this market (remember: when liquidity gets removed from a market, volatility naturally goes up!).

Currently, the BoE hasn’t said if they will extend this “quantitative easing” beyond Friday. In fact, Governor Bailey's speech today (Tuesday) indicated that the operation would be wound down on schedule. However, as you can imagine, there’s certainly a flurry of activity right now at the BoE as they call up pension funds and demand to understand what risks they really have on their books and if any excess leverage can be unwound before Friday.

If the BoE were to withdraw support as planned on Friday and then have another tantrum occur shortly thereafter it would deeply harm market confidence (as it would reflect an inability of the BoE to really understand the risks that exist in markets, thus raising the risk premium associated with all UK assets). This would put more fundamental, along with technical, pressure on gilt yields to move higher. Thus pushing the borrowing costs for a government running excessively large deficits even higher and likely raising the risk premium attached to sterling above its already elevated levels.

It's conceivable – even if it seems contradictory – that we could end up in a dynamic whereby you have the BoE continuing to raise rates (as they need to do, lest sterling further depreciate and thereby import more inflationary pressures) while at the same time they engage in this more technical form of quantitative easing to stop market dislocations from happening. This would put the BoE in a terrible bind, especially since they were planning to start quantitative tightening this month (and were only planning on £80b of tightening over the next twelve months, which is barely more than the £65b they’ve committed, but not yet deployed, through this form of quantitative easing over the past two weeks).

Confidence in UK rates and FX markets are shaken, to put it lightly. Against an energy crisis, headline inflation running around 10%, and extremely soft GDP numbers there is little to cheer about. Especially when compounded by the market expectation that the BoE will raise by 100bps at their next meeting. It’s not an ideal recipe and confidence needs to be restored on both the fiscal and monetary side – even if that involves temporary pain.

Note: Over the past day the BoE has actually purchased a sizeable number of gilts and inflation-indexed gilts (although nowhere close to their limit, £1.4 of the former and £2b of the latter).

Summary

The past few weeks have seen an unprecedented amount of volatility hit the rates market in the UK, and this has reverberated through global markets as folks try to assess whether analogous situations will occur in other countries that are in the midst of their own tightening cycles.

While it’s impossible to give you a full de-brief in just one post, hopefully this has helped laid the stage for you quite well. However, this is a large story and one that will be continuing and will have the potential to impact global rates markets moving forward.

The market is still pricing in significant rate hikes in the UK with GS and others anticipating a 100bps move at the next meeting in November (last week the market was pricing in a 5.5% terminal rate, which I think we’re very unlikely to see). But that goes to show just how far away the market thinks the UK is from getting back to any kind of normalcy.

If you have interviews coming up, this is certainly one market theme you could hit on (although it is evolving quickly, so you may just want to focus on just the original intervention). However, be sure not to get too distracted and focus on more traditional sales and trading interview questions and understanding what sales and trading really involves as well.

Hopefully you’ve found all of this interesting, and be sure to keep tabs on the moves of the BoE over the coming weeks and months. If nothing else, it'll prove to be incredibly interesting and likely quite volatile as well.